No financial plan is complete if it has no mention of an emergency corpus. An emergency corpus acts as shock absorber in times of distress and plays a crucial role in helping you buy time to let things fall into place during a crisis while preventing a spillover effect on your other financial goals. The economic upheaval caused by the coronavirus pandemic has not only served to drive home the point that you can never be completely prepared for any crisis but it has also highlighted how even small steps to secure your finances for any adversity can make a world of difference.

Experts recommend that as a thumb rule your emergency fund should have sufficient capital for you to be able to bear your essential expenses for a period of 6 to 12 months. This fund cannot be used for achieving your other financial goals like buying a car or vacations abroad but neither should it be perceived as building a sizable corpus as is the case with long term goals. The size of the corpus will also depend on your lifestyle and your existing financial liabilities.

Building an emergency corpus is not akin to saving and investing for other financial goals. Unlike retirement or children’s education you cannot stipulate a time frame as to when you would need your emergency corpus. Consequently, the underlying driving force for emergency corpus is not capital appreciation but they are safety and liquidity.

You have to ensure that the invested capital is safe and you can access it easily during the time of need. This automatically eliminates the option of equity investments for this purpose. In the short-term equity investments are highly vulnerable to market volatility triggered by domestic or international events. If you rely on equities for creating your emergency fund, there is no certainty that you will be able to exit from those investments at a profit in times of need. You may be forced to sell your investments at a huge loss if the market conditions are unfavorable at that point of time. Thus there is no point creating an emergency corpus which forces you to look for other financial resources during adverse events.

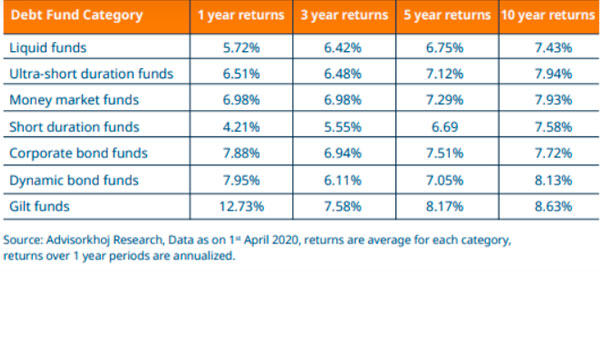

It is for this reason that liquid funds, which are a class of debt funds are considered the best investment avenue for the purpose of building a financial reservoir for rainy days. Liquid funds invest in short‐term assets such as treasury bills, government securities, repos, certificates of deposit, or commercial paper and as per SEBI norms, liquid funds can only invest in debt and money market securities with maturities of up to 91 days. The returns generated by liquid funds depend on the market price of the securities in the fund. Since prices of short-term securities do not fluctuate, it makes liquid funds ideal for emergency fund investments.

A liquid fund typically holds short-term securities that are of good credit quality, and as the name suggests highly liquid. Since investments are only made in short-term securities, risks posed by interest rate changes are negligible and its value remains fairly stable across different interest rate cycles. SEBI directives require liquid funds to only invest in listed commercial paper, and they can only have an overall exposure limit of 20% in a sector. SEBI norms also prohibit liquid funds from investing in risky assets and they must hold a minimum of 20% of their assets in liquid products. Only a small part of the income from liquid funds is generated via capital gains and as an investor you will mostly be earning through interest payments on debt holdings.

Another feature of liquid funds that make them a good fit for building a contingency fund is that there is no lock-in period and you can hold it for as long as required. And unlike FDs, you do not have to worry about paying a hefty tax on your interest income. As an investor in liquid funds, you will not be subjected to any taxes on your dividend income but your capital gains will be subjected to short term and long term capital gains taxes depending on how long you stay invested.

It is important to remember that liquid funds may not be wealth-creating products but they provide adequate safety and liquidity along with decent returns to help you create a solid emergency corpus.

For information on one-time KYC (Know Your Customer) process, Registered Mutual Funds and procedure to lodge a complaint, refer to the knowledge center section available on the website of Mirae Asset Mutual Fund

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

As investors, the journey of investments is a long and a constantly evolving one at that with numerous climaxes and plot points...

Read More...

The right asset allocation mix can provide ample opportunities for investors for tapping into the earning potential of equities while maintaining stability with debt instruments. However, decoding the right asset ...

Read More...

As is the case in our day-to-day lives where we often find ourselves realizing the importance of the axiom that “variety is the spice of life”, in the world of personal finance too, variety has an important place.

Read More...

The growth trajectory of the Indian economy over the last few decades has undoubtedly captured the attention of the world. However, the growth story continues

Read More...

Equity savings funds are open-ended mutual fund schemes in which the investments are spread across equity and debt funds and arbitrage securities.

Read More...

Smart investing is all about finding the right balance between risks and returns. By diversifying your portfolio with the appropriate mix of stable assets

Read More...

With increased focus on the environmental challenges plaguing various countries and communities in the world, there has been a marked shift in the way people are viewing their responsibilities in making the world a better place to live in.

Read More...

Over the last few years, the world of investing has witnessed several shifts in the values that govern investments.

Read More...

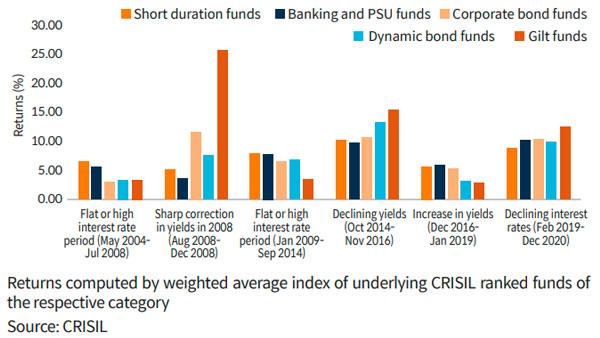

The performance of debt mutual funds is intertwined with interest rate movements as the latter have a significant bearing based on the funds’ yield-to-maturity.

Read More...

Hybrid funds can be an excellent tool for investors to make the best of equity and debt asset classes. They provide ample opportunities for investors for tapping into the earning potential of equities while maintaining stability with investments in debt instruments.

Read More...

Decoding asset allocation can be a daunting task for many investors especially for those who are new to managing investments.

Read More...

A popular English axiom goes: “Variety is the essence of life.” In the world of personal finance too, variety has an important place. Financial planners, investment gurus and fund managers use the term diversification and it is considered one of the building blocks of a successful financial strategy.

Read More...

For many investors, foraying into the journey of investments and gauging the right mix of investment classes can be akin to finding the right ratio of ingredients for baking the perfect cake.

Read More...

>“But what if the market is in a terrible condition when the timeline of my goal is nearing and I am about to redeem my equity investment?” For investors who shy away from equity investments owing to the risks involved, the fear ...

Read More...

The beauty of hybrid fundsis that they come in all shapes and sizes – whether you are a conservative investor or have a high risk tolerance, hybrid schemes afford you the flexibility of maintaining your equity and debt...

Read More...

Dabbling in equities can seem daunting if you are new to the world of investments. Yes, the charm of high returns can seem hard to repel and it may evoke a misplaced sense of...

Read More...

During its second bi-monthly monetary policy review for 2021-2022, the Reserve Bank of India announced that it would be keeping the main policy rates unchanged.

Read More...

My journey in the world of mutual fund investing is marked with phases where I had to teach myself new things and unlearn a lot of preconceived notions about mutual fund investments.

Read More...

In the last few months of 2020, the Indian economy’s recovery from the blows wielded by the first wave of the coronavirus pandemic was stable enough to make market mavericks

Read More...

The resurgence of the coronavirus pandemic has cast doubts on the recovery of India’s economy.

Read More...

In India, fixed deposits continue to dominate the terrain of ‘comfort investments’ for a sizable section of investors. to guaranteed returns and low risks associated with fixed deposit investments, they have been the go-to investment option in India.

Read More...

In October 2020, data from the Association of Mutual Funds showed that debt schemes and corporate bond funds clocked the biggest inflows in more than a year.

Read More...

When investing in a debt instrument, the first consideration ‒ and for many of us the only material one ‒ is the yield to maturity (YTM) it offers.

Read More...

Bank fixed deposits (FDs) have traditionally been the most favoured debt investment option among Indians. But not anymore. With interest rates on FDs falling, especially over the past one year,

Read More...

By investing a fixed amount every month (or any other interval) from your regular savings, you can invest over a long period of time and benefit from the power of compounding.

Read More...

Debt funds are fixed income mutual fund schemes which invest in debt and money market instruments like CPs, CDs, Corporate Bond, T-Bills, G-Secs etc.

Read More...

The equity market's stellar performance has beckoned many investor to take huge exposure to the asset class. Though equity is one of the best wealth creators in the long term, it is prudent to include a less risky asset class such as debt to balance the investment portfolio.

Read More...

Bank fixed deposits and Government small savings schemes have been the traditional investment choice of average Indian households.As per Reserve Bank of India’s Quarterly Estimates of Household Financial Assets and Liabilities, Rs 4,753 billion was invested in bank FDs in FY 2018.

Read More...

In Episode 4 of ‘Winning Over Volatility, we evaluated how banking & PSU funds stand amid the economic downturn, and the dos and don’ts of investing in this category.

Read More..._1593088451941_1593088462624.jpg)

Episode 3 of ‘Winning Over Volatility’ shed light on ETFs and their rising popularity, how they compare to mutual funds, and whether now is the right time to invest in ETFs.

Read More...

In Episode 2 of ‘Winning Over Volatility’, organized in association with Mirae Asset Investment Managers (India) Pvt Ltd., we discussed how one should go about investing in debt funds, especially in light of the current economic downturn.

Read More..._1589893779393_1589893779609.jpg)

Swarup Mohanty, CEO, Mirae Asset Investment Managers (India) Pvt.Ltd, will join us for a discussion on May 22. It will focus on why it’s important to stay invested in the face of a pandemic, and the best way to go about it

Read More...

In the first episode of ‘Winning Over Volatility’, the CEO of Mirae Asset Investment Managers (India) Pvt.Ltd talks about rising investor maturity in India, the 2008 economic crisis, and more.

Read More...

IE Disclaimer

An investor education initiative by Mirae Asset Mutual Fund.

For information KYC process, Registered Mutual Funds and the procedure to lodge a complaint, refer knowledge centre section available on the website of Mirae Asset Mutal Fund.

Mutual fund investments are subject to market risks, read all scheme related documents carefully.