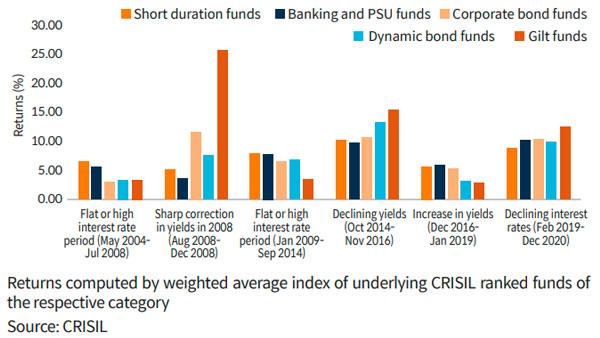

The performance of debt mutual funds is intertwined with interest rate movements as the latter have a significant bearing based on the funds’ yield-to-maturity. The duration of the funds also plays a role in this - debt funds with longer maturity periods are more prone to fluctuations in values due to changes in interest rates than short-term debt funds. Long-term funds have a greater duration and hence the chance is greater that interest rates will vary during its tenure as compared to short or medium-term funds which have a lesser number of interest payments. With shorter–term funds, the chances of drastic movements in interest rates are obviously lower.

Take the case of the financial crisis that rocked global markets in 2008 – yields declined as interest rates plummeted which boosted the performance of longer-duration and medium-to-long duration funds. On the contrary, between December 2016 and January 2019, yields went up and shorter duration funds benefitted. This is because in the case of short-duration funds, the proceeds from the short-term holdings get reinvested at a higher interest rate.

For debt fund investors, especially those who are new entrants to the world of investing, decoding and predicting interest rate trends can be tricky. However, debt funds, unlike equity funds, can provide sufficient returns and stability in a variety of market scenarios if investments in debt funds are made tactfully.

One way to do that is by spreading across investments in various debt fund categories with different maturity periods. For instance, medium-term funds like dynamic bond funds, banking and PSU funds and corporate funds can be great investment vehicles. In the case of corporate bonds the exposure to interest rate volatility is lessened because 80% of assets are invested in high-rated corporate bonds and returns are generated through the accrual of interest on bonds which are held until maturity and are of shorter duration. When it comes to banking and PSU funds, with 80% of the investments being channeled in debt instruments of banks, public sector undertakings, financial institutions and municipal bodies, the credit risk is substantially suppressed. In all these funds, the strategy is to help investors gain the most by striking a balance between mitigating risks and creating returns through accruals. Also, these funds ensure that investors do not have to worry about the credit quality of the underlying investments because investments are made in top-rated instruments.

The Benefits of the SIP RouteMaking investments into debt funds in accordance with prevailing and expected interest rate movements is not only extremely challenging but it can be extremely risky too. Interest rate fluctuations can be triggered by a host of factors, including some unexpected triggers and having an investment strategy that entails timing interest rate changes can be fallacious.

This is where SIPs fit seamlessly into the picture as they allow you to make the most of the potential of debt funds of different types with divergent maturity periods. The SIP in Debt route spares you of the trouble of having to actively track interest rate trends and thus curtails the room for error on the individual investor’s behalf.

With SIPs, you will be investing a fixed amount towards your debt mutual fund every month and thus allows you to reap the advantage of rupee-cost averaging which irons out the bumps created by interest cycles in the long run. When you invest at regular intervals you will end up investing at different prices created by varying market scenarios: you will be allotted units based on the debt fund’s current net asset value (NAV). If the NAV is low, more units are allocated in proportion to the investment amount and when the NAV goes up, lesser mutual fund units are allotted. Hence, it averages the costs at which you purchased units and acts as a buffer against market fluctuations. Additionally with SIPs, you can also inculcate the habit of investing diligently through the investment cycle and you can make the most of your debt fund investments irrespective of the interest rate scenarios.

For information on one-time KYC (Know Your Customer) process, Registered Mutual Funds and procedure to lodge a complaint, refer to the knowledge center section available on the website of Mirae Asset Mutual Fund

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

As investors, the journey of investments is a long and a constantly evolving one at that with numerous climaxes and plot points...

Read More...

The right asset allocation mix can provide ample opportunities for investors for tapping into the earning potential of equities while maintaining stability with debt instruments. However, decoding the right asset ...

Read More...

As is the case in our day-to-day lives where we often find ourselves realizing the importance of the axiom that “variety is the spice of life”, in the world of personal finance too, variety has an important place.

Read More...

The growth trajectory of the Indian economy over the last few decades has undoubtedly captured the attention of the world. However, the growth story continues

Read More...

Equity savings funds are open-ended mutual fund schemes in which the investments are spread across equity and debt funds and arbitrage securities.

Read More...

Smart investing is all about finding the right balance between risks and returns. By diversifying your portfolio with the appropriate mix of stable assets

Read More...

With increased focus on the environmental challenges plaguing various countries and communities in the world, there has been a marked shift in the way people are viewing their responsibilities in making the world a better place to live in.

Read More...

It is common knowledge that the future of our environment is in a precarious position and has become a priority for governments and businesses across the globe.

Read More...

Over the last few years, the world of investing has witnessed several shifts in the values that govern investments.

Read More...

Hybrid funds can be an excellent tool for investors to make the best of equity and debt asset classes. They provide ample opportunities for investors for tapping into the earning potential of equities while maintaining stability with investments in debt instruments.

Read More...

A popular English axiom goes: “Variety is the essence of life.” In the world of personal finance too, variety has an important place. Financial planners, investment gurus and fund managers use the term diversification and it is considered one of the building blocks of a successful financial strategy.

Read More...

For many investors, foraying into the journey of investments and gauging the right mix of investment classes can be akin to finding the right ratio of ingredients for baking the perfect cake.

Read More...

>“But what if the market is in a terrible condition when the timeline of my goal is nearing and I am about to redeem my equity investment?” For investors who shy away from equity investments owing to the risks involved, the fear ...

Read More...

Dabbling in equities can seem daunting if you are new to the world of investments. Yes, the charm of high returns can seem hard to repel and it may evoke a misplaced sense of...

Read More...

No financial plan is complete if it has no mention of an emergency corpus. An emergency corpus acts as shock absorber in times of distress...

Read More...

During its second bi-monthly monetary policy review for 2021-2022, the Reserve Bank of India announced that it would be keeping the main policy rates unchanged.

Read More...

My journey in the world of mutual fund investing is marked with phases where I had to teach myself new things and unlearn a lot of preconceived notions about mutual fund investments.

Read More...

In the last few months of 2020, the Indian economy’s recovery from the blows wielded by the first wave of the coronavirus pandemic was stable enough to make market mavericks

Read More...

The resurgence of the coronavirus pandemic has cast doubts on the recovery of India’s economy.

Read More...

In India, fixed deposits continue to dominate the terrain of ‘comfort investments’ for a sizable section of investors. to guaranteed returns and low risks associated with fixed deposit investments, they have been the go-to investment option in India.

Read More...

In October 2020, data from the Association of Mutual Funds showed that debt schemes and corporate bond funds clocked the biggest inflows in more than a year.

Read More...

When investing in a debt instrument, the first consideration ‒ and for many of us the only material one ‒ is the yield to maturity (YTM) it offers.

Read More...

Bank fixed deposits (FDs) have traditionally been the most favoured debt investment option among Indians. But not anymore. With interest rates on FDs falling, especially over the past one year,

Read More...

By investing a fixed amount every month (or any other interval) from your regular savings, you can invest over a long period of time and benefit from the power of compounding.

Read More...

Debt funds are fixed income mutual fund schemes which invest in debt and money market instruments like CPs, CDs, Corporate Bond, T-Bills, G-Secs etc.

Read More...

The equity market's stellar performance has beckoned many investor to take huge exposure to the asset class. Though equity is one of the best wealth creators in the long term, it is prudent to include a less risky asset class such as debt to balance the investment portfolio.

Read More...

Bank fixed deposits and Government small savings schemes have been the traditional investment choice of average Indian households.As per Reserve Bank of India’s Quarterly Estimates of Household Financial Assets and Liabilities, Rs 4,753 billion was invested in bank FDs in FY 2018.

Read More...

In Episode 4 of ‘Winning Over Volatility, we evaluated how banking & PSU funds stand amid the economic downturn, and the dos and don’ts of investing in this category.

Read More..._1593088451941_1593088462624.jpg)

Episode 3 of ‘Winning Over Volatility’ shed light on ETFs and their rising popularity, how they compare to mutual funds, and whether now is the right time to invest in ETFs.

Read More...

In Episode 2 of ‘Winning Over Volatility’, organized in association with Mirae Asset Investment Managers (India) Pvt Ltd., we discussed how one should go about investing in debt funds, especially in light of the current economic downturn.

Read More..._1589893779393_1589893779609.jpg)

Swarup Mohanty, CEO, Mirae Asset Investment Managers (India) Pvt.Ltd, will join us for a discussion on May 22. It will focus on why it’s important to stay invested in the face of a pandemic, and the best way to go about it

Read More...

In the first episode of ‘Winning Over Volatility’, the CEO of Mirae Asset Investment Managers (India) Pvt.Ltd talks about rising investor maturity in India, the 2008 economic crisis, and more.

Read More...

IE Disclaimer

An investor education initiative by Mirae Asset Mutual Fund.

For information KYC process, Registered Mutual Funds and the procedure to lodge a complaint, refer knowledge centre section available on the website of Mirae Asset Mutal Fund.

Mutual fund investments are subject to market risks, read all scheme related documents carefully.